Audit and Accounting in Hungary

Your consultant

Alina Marinich

Senior Business Consultant

Accounting in Hungary is our specialty, and with many years of experience in servicing various organizations, coupled with the expertise of our employees, we are able to solve any professional tasks with maximum benefit for our customers.

Since self-accounting takes a lot of time, and it is expensive to maintain a full-time accountant, we can offer you both one-time services and full professional accounting support for your company.

Qualified personnel who are ready to take care of the bookkeeping and tax accounting of your foreign company, as well as cooperation with independent auditors and with the tax authorities of other states at your disposal.

Accounting in Hungary: General Information for Companies

As the Act C of 2000 on Accounting says, companies registered in Hungary must keep accounting records that provide an accurate and complete picture of the company’s state of affairs, being the major instrument of knowledge, management and control.

Accounting records and the financial report have to be prepared in Hungarian.

As a EU Member State, Hungary is subject to accounting, auditing and financial reporting requirements set out in EU Rules and Directives as implemented into national laws and regulations.

In particular, Hungarian companies should prepare their financial statements in accordance with IFRS.

All Hungarian economic entities shall keep double-entry books.

Companies shall keep accounts of all economic events, the effect of which on the assets and liabilities, as well as on profits are to be shown in the financial report.

The financial report shall give a true and fair view of the financial position and performance of the economic entity, including any changes therein.

Depending on the amount of annual net sales revenues, the balance sheet total, the number of employees, and the limits thereof Hungarian companies are allowed to prepare different types of financial reports:

- annual account,

- simplified annual account,

- consolidated annual account,

- simplified report.

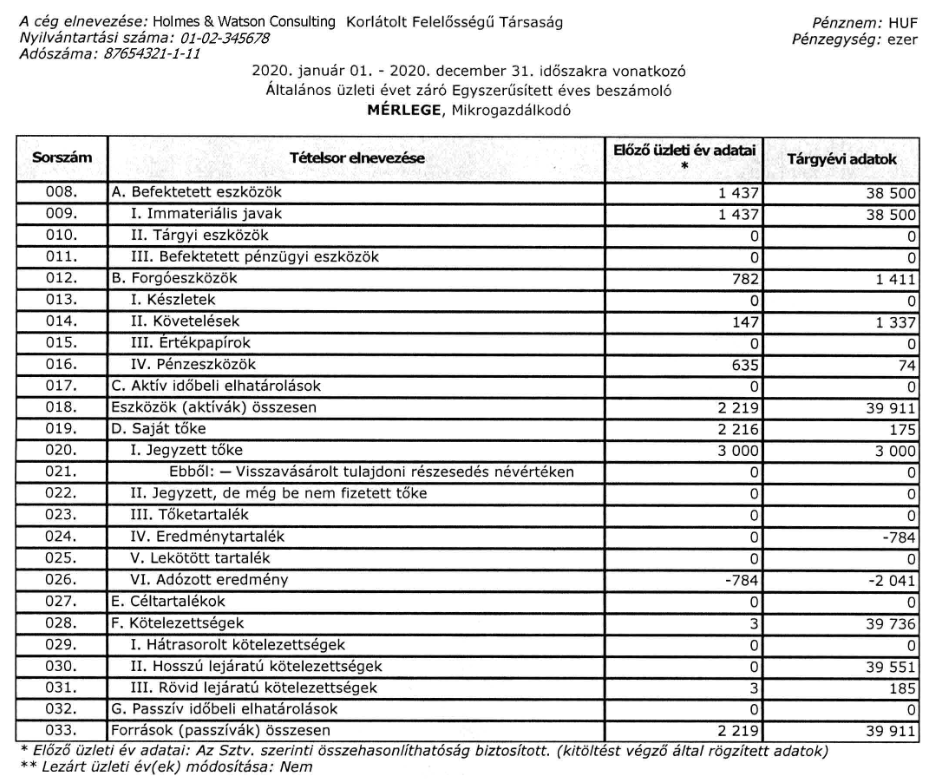

The annual accounts usually include:

- the balance sheet,

- the profit and loss account,

- notes on the accounts,

- audit report, if required,

- and the annual report.

Economic entities may prepare a simplified annual account if, on the balance sheet date in two consecutive financial years, two of the following three size-related indices do not exceed the limits indicated below:

- the balance sheet total does not exceed HUF 1.200.000.000 (~ EUR 3.280.000);

- the annual net sales revenue does not exceed HUF 2.400.000.000 (~ EUR 6.560.000);

- the average number of employees in the financial year does not exceed 50 persons.

Companies that meet two of the following three thresholds may prepare a simplified annual report:

- balance sheet total of less than HUF 500.000.000 (~ EUR 1.365.000);

- annual net revenue less than HUF 1.000.000.000 (~ EUR 2.735.000); or

- average number of employees during the business year is 50.

The simplified report consists of the simplified balance sheet and the profit and loss statement.

You are advised to ask your consultant to determine which type of financial report should be prepared for your company.

The auditing of accounting documents shall not be statutory if both of the conditions below are satisfied:

- the company’s annual net sales did not exceed HUF 300.000.000 (~ EUR 820.000) on the average of the two financial years preceding the financial year under review, and

- the average number of employees of the company of the two financial years preceding the financial year under review did not exceed 50 persons.

Please connect your consultant on the necessity of an audit and the volume of financial statements.

We provide the following accounting services in Hungary:

- Inspection of the provided documents for completeness and compliance with the company’s business activities;

- formation of a set of supporting documents to be provided to auditor; for the company’s archive;

- preliminary assessment of the financial result and forecast of the amount of liabilities for corporate tax, VAT, etc.;

- preparation of accounts, formation of profit and loss statement and balance sheet in accordance with IFRS and corporate legislation;

- preparation and submission of accounting statements based on the provided supporting documents;

- by additional client’s request:

- keeping accounting records of the company with the provision of interim financial results on a monthly, quarterly or semi-annual basis.

Сonsolidated Financial Statements

The parent Hungarian company shall not be required to draw up consolidated annual accounts on the financial year if, on the balance sheet date in two consecutive years preceding the current financial year, two of the following three indices do not exceed the following limits:

- The balance sheet total does not exceed HUF 6.000.000.000 (~ EUR 16.400.000);

- The annual net sales revenue does not exceed HUF 12.000.000.000 (~ EUR 32.800.000);

- The average number of employees in the financial year does not exceed 250 persons.

We also provide services for the preparation of consolidated financial statements for a group of companies, if this is required in accordance with the Act C of 2000 on Accounting or in accordance with your request.

When preparing consolidated financial statements, if necessary, you can also use our services to audit the operations of subsidiaries registered in other jurisdictions.

Submission Deadlines

The financial year usually coincide with the calendar year. However, pursuant to the Accounting Act, taxable persons may exercise discretion in deciding on the operation of a financial year differing from the calendar year, especially if it is made reasonable by the characteristics of operation.

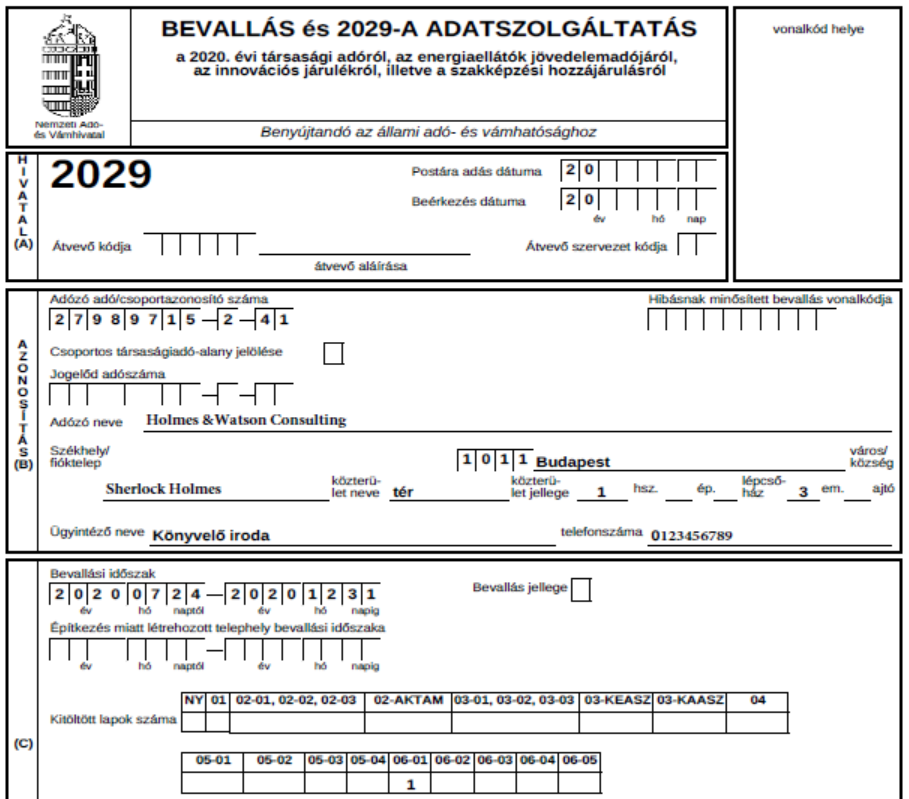

The annual accounts and corporate tax return shall be filed by taxpayers operating according to the calendar year by 31 May of the year following the tax year. In case of taxpayers opting for a business year other than the calendar year, a return shall be filed until the last day of the fifth month following the last day of the tax year.

The overdue filing of a company’s accounts is subject to a late filing fee.

You are advised to refer to your consultant in order for him to orient you on individual deadlines of your company for filing due date of the company’s accounts.

Tax Filing Requirements

The incomes deriving both from Hungary and abroad of resident taxable persons shall be subject to tax.

Foreign companies conducting entrepreneurial activities in premises in Hungary shall pay tax on their income deriving from their entrepreneurial activities conducted in premises in Hungary.

The corporate tax rate is 9% of the positive tax base.

We are ready to assist you in the preparation of calculations of the estimated profit for the current year as well as the assessment of tax liabilities for corporation tax and other taxes.

To determine the tax burden of the company, we recommend consult with a tax consultant

VAT Returns

It is also necessary to take into account vat-related issues. In most EU countries, including Hungary, VAT registration obligations do not arise as long as the sales turnover in the country is below the registration threshold, which is HUF 12.000.000 (~ EUR 32.800). At the same time, initiative registration is possible.

The general VAT rate in Hungary is 27%.

The VAT returns must be submitted on a monthly basis. However, depending on the value limit, the reporting frequency further on may be annual or quarterly.

In cases of non-submission and/or late submission of VAT returns, a default penalty may be levied.

If your Hungarian company no longer needs to be registered for VAT due to a change in the direction of activity, or due to the termination of activity, or for any other reason, we also provide services for de-registering the company with VAT in accordance with the current Hungarian corporate and tax legislation.

How Can Our Hungary Accountants and Auditors Help?

We offer a comprehensive suite of services, including the preparation of accounting and tax reports, audit and submission of accounts to Hungarian public authorities, and full administrative support for our clients’ offices in Hungary, all supported by our expertise in accounting services in Hungary and Hungary audit services

Having our own presence in Hungary since 2018, we have acquired a unique practice of direct cooperation on the issues of our clients’ companies with government institutions.

Consult with Experts Before You Begin

Since Hungary does not belong to offshore jurisdictions, and a Hungarian company is obliged to submit reports and pay taxes on a regular basis in accordance with the procedure established by law, before starting the registration of a Hungarian company, we recommend that you get advice from lawyers and auditors regarding the subsequent administration of the company.

BASIC FEES FOR OUR SERVICES

| SERVICES | PRICE[1] |

| Monthly accounting services | |

| Preparation and submission of the VIES declaration

Preparation of a trial balance |

from 200 EUR

from 250 EUR |

| Quarterly accounting services | |

| Preparation and submission of VAT declaration | from 400 EUR |

| Yearly accounting services | |

| Preparation and submission of an annual report | from 1.200 EUR |

| Statutory audit | 100-350 EUR per hour of work |

| Additional services | |

| VAT registration | 1.200 EUR |

| VAT de-registration | 1.200 EUR |

| Consultations, communication with auditors and government agencies | 100-350 EUR per hour of work |

[1] The price is shown without VAT. UAE VAT rate – 5%.