Audit and Accounting Services in Cyprus

Your consultant

Alina Marinich

Senior Business Consultant

The expertise of our Cyprus chartered accountants, combined with extensive experience in serving diverse organizations, empowers us to efficiently address any professional challenge while ensuring maximum benefits for our clients.

Since self-accounting takes a lot of time, and it is expensive to maintain a full-time accountant, we can offer you both one-time services and full professional accounting support for your company.

Qualified personnel who are ready to take care of the bookkeeping and tax accounting of your foreign company, as well as cooperation with independent auditors and with the tax authorities of other states at your disposal.

Essential Accounting and Financial Guidelines for Businesses in Cyprus

The management of all companies registered in Cyprus shall cause to be kept books of accounts and records, which are considered necessary for the preparation of financial statements which shall correctly explain all the transactions and enable the determination of the financial position of the company with reasonable accuracy at any given time.

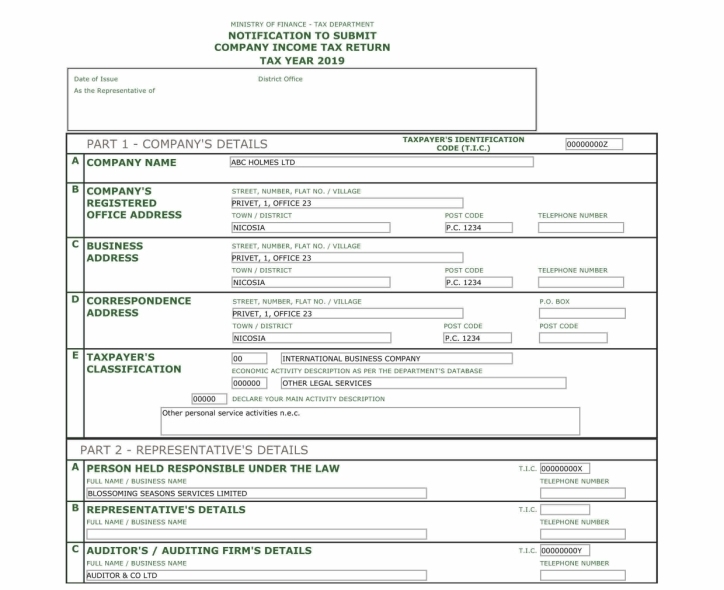

According to Article 142 of The Companies Law (Cap. 113), Cypriot companies are required to prepare and submit financial statements certified by an auditor in accordance with International Financial Reporting Standards. This requirement is mandatory regardless of whether the company has been operating or not.

The financial statements must include:

- Profit and loss account;

- Balance Sheet signed by at least two (2) directors;

- Notes;

If the activity was not carried out, the company’s auditors must prepare and submit Dormant Audited Financial Statements.

Combined Financial Reports

Each Cypriot company which has subsidiaries shall consolidate its financial statements with the financial statements of its subsidiaries.

However, ‘small sized groups’ shall be exempt from the obligation to prepare consolidated financial statements.

A group of companies is classified as small if the following conditions are met:

- the companies subject to consolidation are not public;

- the preparation of their consolidated financial statements is not governed by any other legislation;

- the companies satisfy at the date of closing of the balance sheet of the parent company, two of the following three criteria:

- The total of the assets appearing in the balance sheet does not exceed the amount of EUR 17.500.000;

- The net level of the turnover does not exceed the amount of EUR 35.000.000, and

- The average number of employees at the relevant period does not exceed 250.

We also provide services for the preparation of consolidated financial statements for a group of companies, if this is required in accordance with the standards of The Companies Law (Cap. 113) or in accordance with your request.

When preparing consolidated financial statements, if necessary, you can also use our services to audit the operations of subsidiaries registered in other jurisdictions.

Key Submission Dates for Financial Reports

Financial statements shall be presented at the latest eighteen months after the incorporation of the company and subsequently once at least in every calendar year.

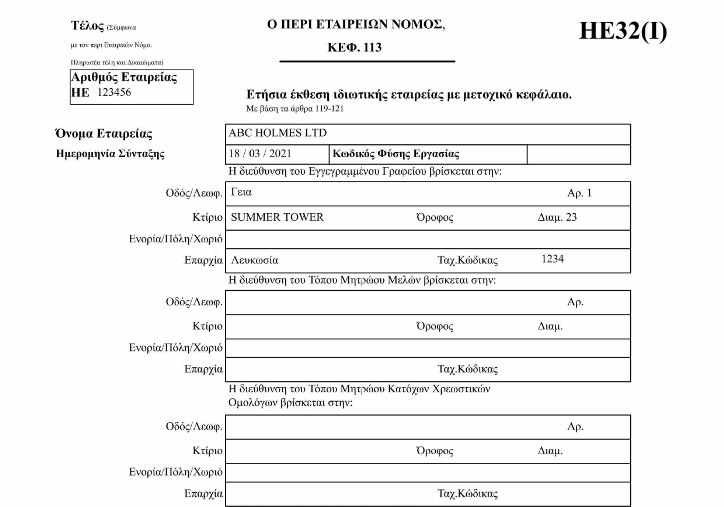

Every company draws up an Annual Return (HE32 Form) once every calendar year which includes, essential information about the company as at the date of its drafting. The Annual Return is accompanied by the Financial Statements relating to the previous financial year.

The Annual Return accompanied with the Financial Statements must be made up to a date until the company’s Annual Return Date and, must be filed at the Department of the Registrar of Companies within twenty-eight (28) days from its drafting date.

The overdue filing of an Annual Return and the Financial Statements is subject to a late filing fee.

As part of our accounting services in Cyprus, we advise you to refer to our consultant so they can guide you on the individual deadlines for your company regarding the filing due date of the Annual Return.

Tax Compliance Services

In addition to annual reports a company that is a tax resident of Cyprus is taxed on income received or derived from all taxable sources in Cyprus and abroad.

For all companies, the income tax rate is 12,5%.

The tax return must be submitted to the Inland Revenue Department within 12 months after the end of the reporting period, i.e. before December 31 of the year following the reporting one, while for electronic forms of filing declarations, the specified period has been extended by three months.

The tax return must be certified (and actually prepared) by the company’s auditor.

Our Cyprus tax accountants are ready to assist you in the preparation of calculations of the estimated profit for the current year as well as the assessment of tax liabilities for corporation tax and other taxes.

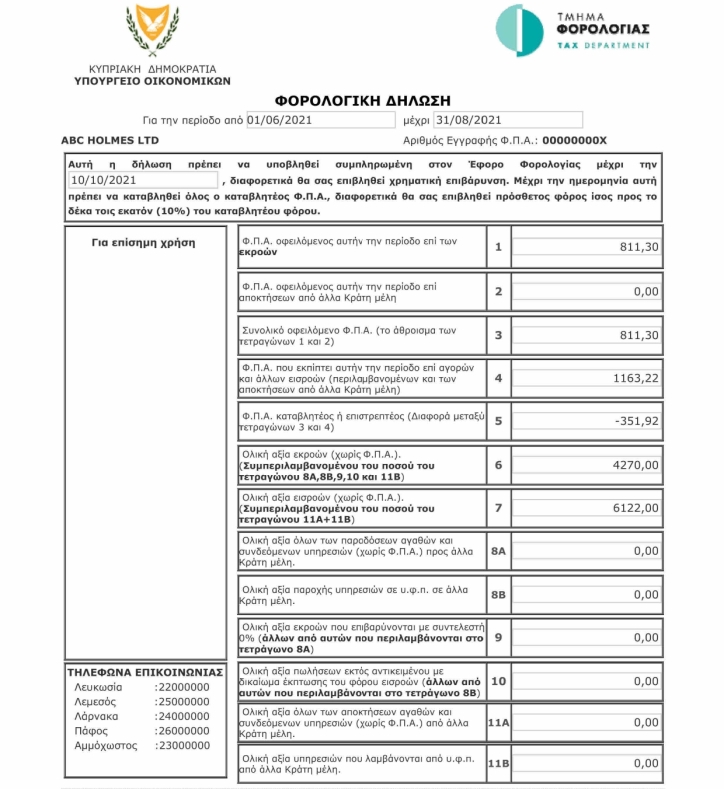

VAT Returns

It is also necessary to take into account vat-related issues. In most EU countries, including Cyprus, VAT registration obligations do not arise as long as the sales turnover in the country is below the registration threshold, which in Cyprus is EUR 15.600. At the same time, initiative registration is possible.

The VAT rate in Cyprus is 19%.

If you Cypriot Company no longer needs to be registered for VAT due to a change in the direction of activity, or due to the termination of activity, or for any other reason, we also provide services for de-registering the company with VAT in accordance with the current Cypriot corporate and tax legislation.

Our Cyprus Services

We offer comprehensive Cyprus audit and tax services, alongside Cyprus accounting services, to ensure full compliance with local regulations. Our expertise also includes accounting supervision services in Cyprus, providing tailored support for the preparation of accounting and tax reports, conducting audits, submitting audited statements to public authorities, and offering administrative assistance for our clients’ offices in Cyprus.

Having our own presence in Cyprus since 2006, we have acquired a unique practice of direct cooperation on the issues of our clients’ companies with government institutions, such as Registrar of Companies, Inland Revenue Department, VAT Service, The Department of Customs and Excise, Civil Registry and Migration Department, Social Insurance Department and others.

Consult with an Expert Before You Begin

Since Cyprus does not belong to offshore jurisdictions, and a Cyprus company is obliged to submit reports and pay taxes on a regular basis in accordance with the procedure established by law, before starting the registration of a Cyprus company, we recommend that you get advice from lawyers and auditors regarding the subsequent administration of the company.

Auditor or internal revenue service staff, Business women checking annual financial statements of company. Audit Concept

Basic Fees for Our Cyprus Services

| SERVICES | Fee [1] |

| Monthly accounting services | |

| Preparation and submission of the VIES declaration | 100-350 EUR per hour |

| Quarterly accounting services | |

| Preparation and submission of VAT declaration | 100-350 EUR per hour |

| Yearly accounting services | |

| Preparation and submission of Dormant Company Audited Report (for companies that did not operate in the reporting period) | 1.140 EUR |

| Preparation and submission of reports for a company that has started operating | 100-350 EUR per hour |

| Additional services | |

| VAT registration | 1.200 USD |

| VAT de-registration | 1.200 USD |

| Consultations, communication with auditors and government agencies | 100-350 EUR per hour |

[1] The price is shown without VAT. UAE VAT rate – 5%.